Office Hours

By Appointment

Our Location

617 Cherokee Ct, Davenport IA 52804

Call Us Now

(866) 440-1885

Still have questions?

Get in touch with us

Medigap (aka Medicare Supplement Plans)

|

|

|

|

|

|

|

|

|

Important Points

Medigap plans help individuals pay for the remaining expenses that Medicare leaves them liable for.

There are 10 Medigap plans on the market. each with a uniform coverage regardless of the insurance company you select.

You must be enrolled in Medicare Part A & Part B in order to purchase a Medigap plan.

Medicare Supplement (Medigap) plans help pay for your share of Medicare expenses, such as deductibles and co-insurance. Medigap plans are available for purchase in all 50 states and are popular with individuals who want little to no copays when they access healthcare services.

Medicare itself only covers 80% of your Part B expenses, while you cover the other 20%. That 20% can be financially devastating if you happen to get a serious illness. You can choose Medigap plans that will pay some or even all of that 20% for you. Medigap plans essentially buy you peace of mind by eliminating your cost-sharing responsibility.

During your one-time open enrollment window, you are guaranteed the right to purchase a Medigap plan. It is the only time that you can get a Medigap plan without having your age or health status taken into consideration.

Mohring Insurance Services LLC | Talk to a Medicare Expert at (866) 440-1885

What is Medigap?

Medigap policies were created shortly after Medicare was signed into law. Due to the fact that you are required to pay for some things, like 20% of your outpatient expenses, Medigap policies were created to pay those expenses for you. This allows you to feel less worried about how much each medical visit will end up costing you.

Some of the advantages of a Medigap policy are:

Freedom to choose your own doctors and hospitals

Guaranteed renewability - the insurance carrier can never drop you or change your coverage due to a health condition

Nationwide coverage - you can use your plan anywhere in the United States

No referrals are required to see a specialist

Predictable out-of-pocket expenses for Medicare covered services (almost no out-of-pocket with Plan G)

A Medigap plan is the most predictable secondary coverage you can buy. You will know exactly what is covered for every inpatient and outpatient procedure based on which Medigap plan you choose.

Here are some other things to know about a Medigap plan:

You must have Medicare Part A & B in order to buy a Medigap policy.

Medigap plans cover only one person. Your spouse must have their own individual policy.

You can drop your Medigap plan at any time. There is no annual election period for Medigap plans.

The Annual Election Period in the fall is for prescription drug plans. It does not apply to Medigap plans in any way.

Some carriers offer household discounts if two or more people enroll in a Medigap plan from the same company.

Medigap plans do not include Part D prescription drug coverage, so you'll need to purchase a separate stand-alone Part D drug plan.

Medigap Plan Coverage

Medigap plans pay out after Medicare approves and pays its share of your claim. It is literally gap coverage, helping to cover the gaps in Medicare that you would normally have to pay. This includes costs such as deductibles, coinsurance, and copays.

You can use your Medigap plan at any provider in the country that accepts Medicare. This makes a Medigap plan great for travelers or people who live in more than one state throughout the year.

It is important to know that Medigap plans do not include prescription drug coverage, so you will want to purchase a separate standalone Part D drug plan for your medications. A Medigap policy also does not cover routine dental, vision, or hearing services. Therefore, you may need to look into purchasing a separate policy for these services if you are interested in having them.

Medigap - Uniform Coverage

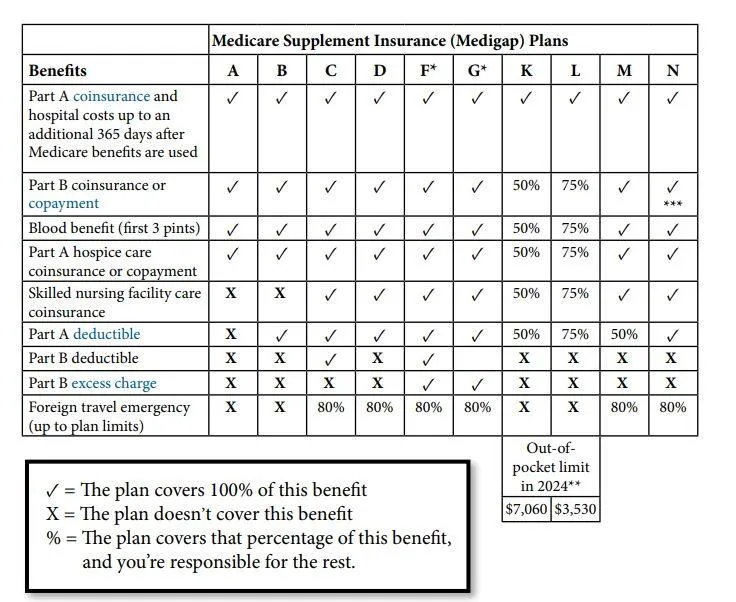

For a list of all of the Medigap plans available, take a look at our Medicare Supplement Plan chart below. This chart details the benefits covered by each different Medigap plan.

Some people have found that Medigap coverage can be difficult to understand, so on our site, we have tried to use simple terms. Our pages on the different Medigap plans include examples of how the coverage would pay. This can help you understand how they would work in real situations.

Medigap Plan F and Plan G also offer high-deductible plans (HDF or HDG) by some insurance carriers in some states. If you choose to enroll in a high-deductible option, it means that you must pay for Medicare-covered costs (coinsurance, deductibles, copayments) up to the deductible amount of $2,870 in 2026 before your policy will pay anything.

For Medigap Plans K and L - After you meet your annual out-of-pocket limit and your annual Part B deductible ($257 in 2026), the Medigap plan pays 100% of covered services for the rest of that calendar year.

Plan N pays 100% of the Part B coinsurance, except for a copay of up to $20 for some office visits and up to a $50 copay for emergency room visits that do not result in an inpatient admission to the hospital.

What are my Medigap Plan Choices?

Each Medigap plan in the chart above has a letter, A - N. Each plan letter is a different type of plan that provides a different set of benefits. Each lettered plan must offer the same set of uniform coverage regardless of where you get it. For instance, Medigap Plan G at Aetna has the same benefits as Plan G from Humana. There are 10 standardized Medigap plans that can be offered by insurance companies in most states.

There is one Medigap plan that covers nearly ALL of the gaps, leaving you with only your Part B deductible - Plan G. There are others where you agree to do some cost-sharing and in return, you get a lower monthly premium. If you prefer something in the middle you could look at Plan N where you pay for a few things yourself in exchange for lower premiums.

An insurance agent specializing in Medicare products can help determine which plan best suits you.

How do I Choose a Medigap Plan?

Most people enroll in Plan G or Plan N, although there are many other options. This is because these two plans offer the most coverage. However, the reason you have choices is so you can decide what is most important to you. Some individuals prefer a plan that covers all the gaps and leaves them with no anxiety about the cost of medical procedures. Other people prefer a plan where only some of their cost-sharing is covered in order to pay a lower monthly payment.

There is no right or wrong answers here. As your agent to provide quotes for several plans to see what makes the most sense to you.

Medigap - Open Enrollment

Medicare Advantage PPO plans are just one option you have for your Medicare insurance coverage. These are not the same as Medigap plans. The cost and coverage is different, so you will want to understand both types of plans before you make your choice.

Choosing a plan can be daunting. You need to ensure that you will have access to your doctors and the medications that you require. One of our licensed agents that specialize in Medicare plans can do this research for you at no cost. When you enroll with us, we provide support to you when you have questions about how your benefits will pay for certain services or claims. For a free 1-on-1 consultation call us at (866) 440-1885 to determine whether a Medicare PPO plan would be best for you.

Key Points

PPO plans allow you to go out of network. However, you will likely pay higher costs.

Many PPO plans have low or even $0 premiums.

Many PPO plans have built-in Part D prescription drug coverage at no extra cost to you.

Your plan benefits can change from year to year. Review your Annual Notice of Change (ANOC) letter each September.

At Mohring Insurance Services LLC, we are happy to offer assistance with Medicare when you choose to enroll. Give us a call at (866) 440-1885, or to schedule a free consultation, click the link below:

© 2026 Mohring Insurance Services LLC All Rights Reserved.

MyMedicareFacts.com is a free-to-use information website by Mohring Insurance Services LLC. All insurance agents and enrollment platforms linked to this site have their own terms and conditions.

This is a promotional communication.

Calling our phone number will connect you to a licensed broker who is trained and certified to help you review the plan options available in your area. We do not offer every plan available in your area. Any information we provide is limited to those plans we do offer in your area. Please contact MEDICARE.gov or 1-800-MEDICARE to get information on all your options.

Not all plans offer all of these benefits. Benefits may vary by carrier and location. Limitations and exclusions may apply.

To send a complaint to Medicare, call 1-800-MEDICARE (TTY users should call 1-877-486-2048), 24 hours a day / 7 days a week). If your complaint involves a broker or agent, be sure to include the name of the person when filing your grievance.

MyMedicareFacts.com is the web and phone-based insurance portal utilized by Mohring Insurance Services LLC. Beneficiaries may be connected by licensed insurance agents of Mohring Insurance Services LLC who are licensed to transact business as insurance agents in your state.

Not all licensed insurance agents with Mohring Insurance Services LLC are licensed to sell all products. Service and product availability varies by state. Agents of Mohring Insurance Services LLC work with Medicare enrollees to explain Medicare Advantage, Medicare Supplement Insurance, and Prescription Drug Plan options. Agents of Mohring Insurance Services LLC are licensed and certified representatives of Medicare Advantage HMO, PPO, and PPFS organizations and stand-alone prescription drug plans. Each of the organizations we represent has a Medicare contract. Enrollment in any plan depends on contract renewal.

Licensed insurance agents may be compensated based on a consumer's enrollment in a health plan. No obligation to enroll. Licensed agents cannot provide tax or legal advice. Contact your tax or legal professional to discuss details regarding your individual business circumstances. Our quoting tool is provided for your information only. All quotes are estimates and are not final until consumer is enrolled.

Please call our customer service number or see your Evidence of Coverage for more information, including the cost sharing that applies to out-of-network services.

Medicare has neither reviewed nor endorsed this information.

Licensed insurance agents required to comply with all applicable federal laws, including the standards established under 45 C.F.R. § 155.220(c) and (d) and standards established under 45 C.F.R. § 155.260 to protect the privacy and security of personally identifiable information.

The plans we represent do not discriminate on the basis of race, color, national origin, age, disability, sex, sexual orientation, gender identity, or religion. To learn more about a plan’s nondiscrimination policy, please contact the plan.

For a complete list of available plans please contact 1-800-MEDICARE, TTY 711, 24 hours a day/7 days a week or consult www.medicare.gov.

Medicare beneficiaries may also enroll through the CMS Medicare Online Enrollment Center located at www.medicare.gov.

Every year, Medicare evaluates plans based on a 5-star rating system.

You are not required to provide any health related information unless it will be used to determine enrollment eligibility.

MyMedicareFacts.com is not connected with or endorsed by the United States government or the federal Medicare program.

© Mohring Insurance Services LLC. All trademarks and service marks are the property of their respective owners and used with permission.

Rates are reviewed periodically and are subject to change in your state.

Cost Estimates are based on the information entered, using data about past experiences by beneficiaries with similar attributes and the premiums and benefits provided by the plan. Actual costs may vary. Monthly medical costs are represented by annual figures divided evenly per month.

Licensed sales agents/producers may be compensated based on your enrollment in a health plan.

Medicare Supplement Plans are not connected with or endorsed by the U.S. Government or the federal Medicare program.

For plans that provide drug coverage, the formulary may change during the year.

Medicare beneficiaries may also enroll in Medicare plans through the CMS Medicare Online Enrollment Center located at https://www.medicare.gov.